Will UK Interest Rates Fall in 2026? Latest Bank of England Forecast

UK interest rates remain one of the most important topics for homeowners, investors, savers, and businesses across Britain. As inflation, mortgage costs and economic uncertainty continue to affect household finances, many people are asking the same question: Will UK interest rates fall in 2026?

Thank you for reading this post, don't forget to subscribe!The short answer is that rate cuts are still possible, but the outlook has become more complicated. While inflation eased earlier in the year, recent energy price pressures and global geopolitical tensions have increased uncertainty around future Bank of England decisions.

UK Interest Rates in 2026: Quick Answer

Will UK interest rates fall in 2026?

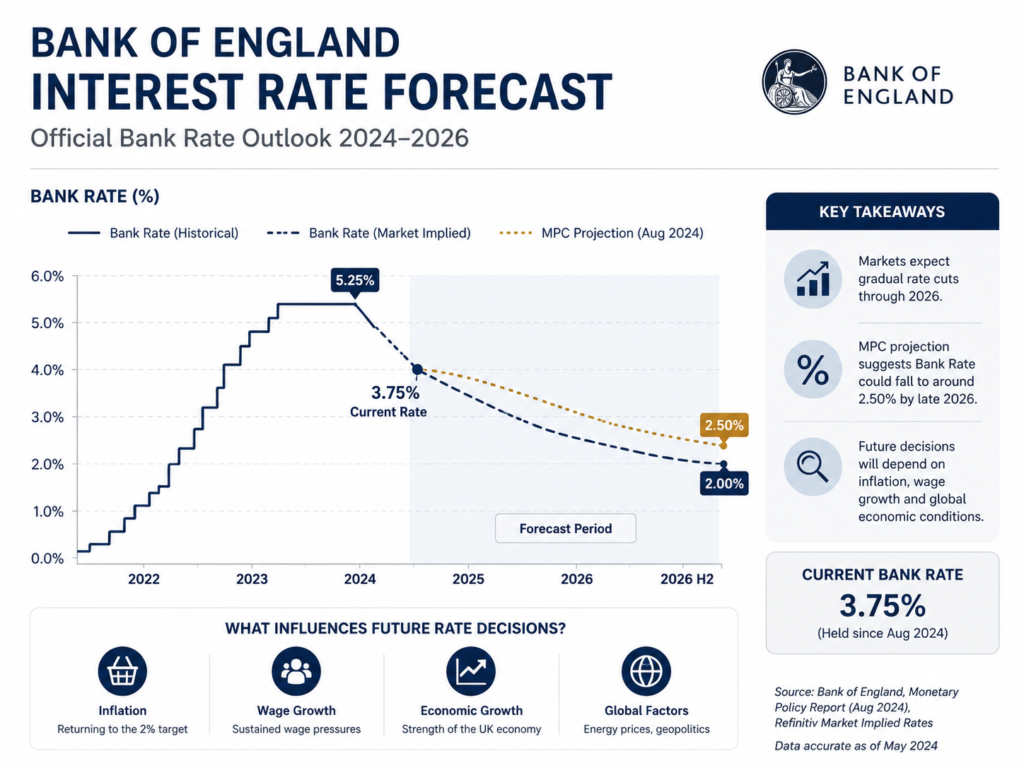

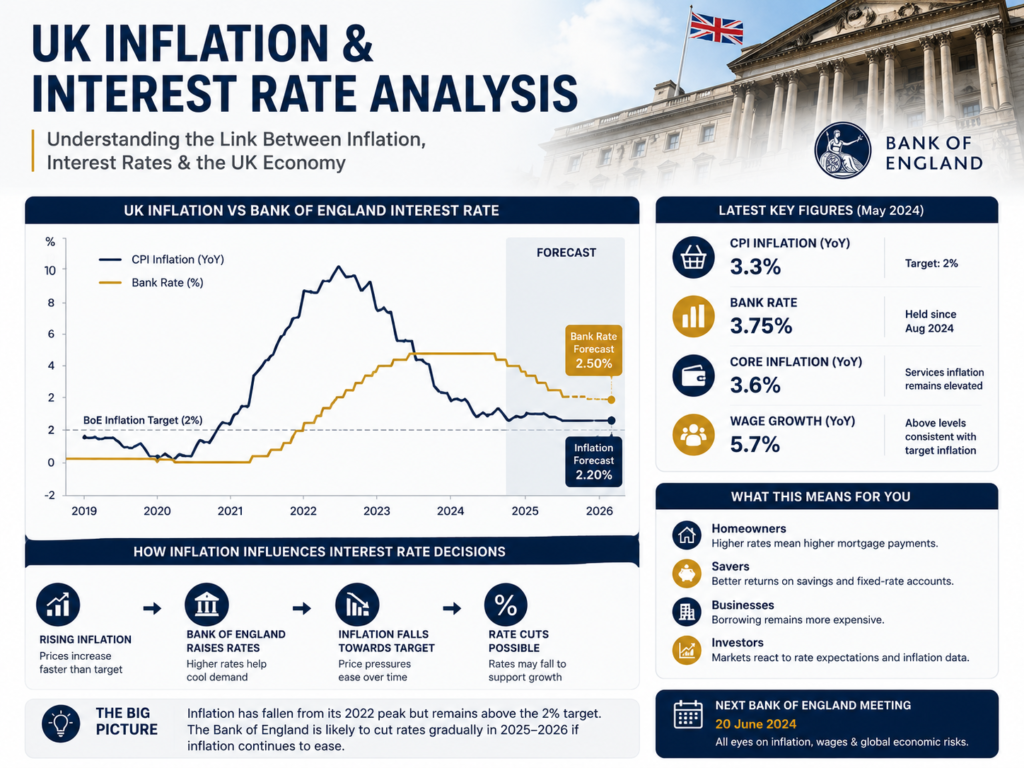

The Bank of England has recently held the Bank Rate at 3.75%, but policymakers remain divided on the next move. Some experts believe rates could gradually fall if inflation continues moving closer to the Bank’s 2% target. Others warn that persistent inflation could keep rates higher for longer.

For now, markets expect cautious decisions rather than aggressive rate cuts.

Current Bank of England Interest Rate

The current Bank Rate stands at 3.75% following recent Monetary Policy Committee decisions. The Bank has chosen to keep rates unchanged while monitoring inflation, wage growth and broader economic conditions.

The Bank of England’s main objective remains:

- Keeping inflation near 2%

- Maintaining economic stability

- Supporting sustainable growth

Interest rate decisions are reviewed eight times per year.

Why UK Interest Rates Matter

UK interest rates influence almost every part of the economy.

For homeowners

Interest rates affect:

- Mortgage repayments

- Remortgaging costs

- Housing affordability

For savers

Higher rates often lead to:

- Better savings account returns

- Improved fixed-rate bond offers

For businesses

Borrowing costs impact:

- Business expansion

- Hiring decisions

- Investment spending

For investors

Interest rates influence:

- Stock market valuations

- Bond yields

- Property investments

Why UK Interest Rates Rose in Recent Years

The Bank of England increased rates aggressively during the inflation surge that followed:

- Supply chain disruptions

- Rising energy costs

- Labour shortages

- Global economic instability

The goal was to reduce inflation by slowing demand across the economy.

Although inflation has fallen significantly from previous highs, it remains above the Bank’s long-term target.

Will UK Interest Rates Fall in 2026?

This is currently one of the most searched financial questions in Britain.

The answer depends largely on three factors:

1. Inflation

Inflation remains the biggest driver of future rate decisions.

The Bank recently stated that inflation has risen to around 3.3%, above its 2% target. Energy prices and global events continue creating uncertainty.

If inflation falls consistently:

- Rate cuts become more likely.

If inflation rises again:

- Rates could remain unchanged or even increase.

2. Wage Growth

The Bank closely monitors wages.

Strong wage growth can increase spending power, which may keep inflation elevated.

Recent data shows policymakers remain cautious about wage-driven inflation pressures.

3. Economic Growth

The UK economy has shown signs of slowing.

Weak growth may encourage future rate reductions if inflation risks decrease.

However, the Bank must balance growth concerns against inflation control.

Latest Bank of England Forecast

The Bank of England recently indicated that inflation could remain elevated during parts of 2026 because of energy market uncertainty. Officials have stressed that future policy decisions will depend on incoming economic data rather than a fixed timeline.

Several Monetary Policy Committee members have already voted for rate reductions in previous meetings, suggesting there is growing support for eventual cuts if inflation improves further.

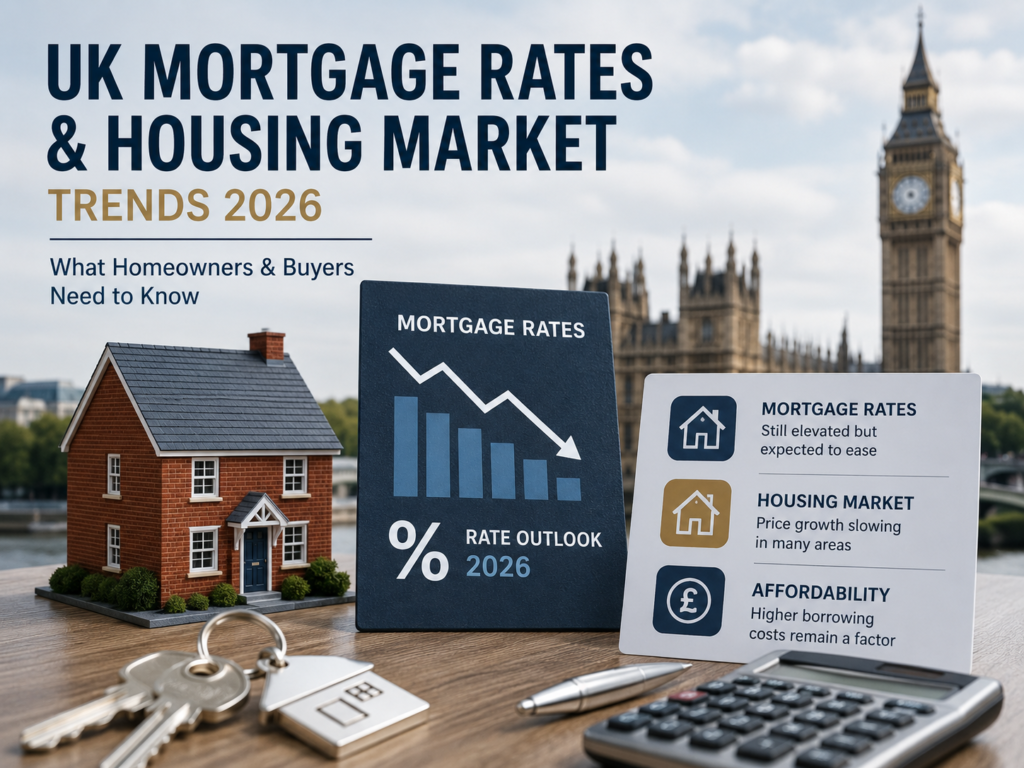

How UK Interest Rates Affect Mortgages

Mortgage holders remain particularly sensitive to Bank Rate changes.

If rates fall:

Potential benefits include:

- Lower monthly repayments

- Improved remortgaging deals

- Better affordability for first-time buyers

If rates stay high:

Borrowers may continue facing:

- Expensive fixed-rate deals

- Higher borrowing costs

- Reduced housing affordability

Recent reports suggest mortgage rates remain elevated compared to pre-inflation years.

How UK Interest Rates Affect Savings Accounts

Higher rates have benefited savers over the past few years.

Savings advantages:

- Better fixed-rate accounts

- Improved ISA returns

- Stronger cash savings yields

However, if rates eventually fall:

- Savings returns may decline

- Banks could reduce account rates

This is why many savers are watching Bank of England announcements closely.

UK Interest Rates and the Housing Market

The property market is closely linked to borrowing costs.

Recent housing reports show:

- Slower house price growth

- Higher mortgage costs

- Reduced buyer demand

Some analysts believe lower rates could support housing activity later in 2026 if inflation eases further.

Impact on Businesses and Investments

Businesses often delay expansion when borrowing becomes expensive.

Higher rates can affect:

- Startup funding

- Corporate investment

- Commercial property demand

Investors also monitor interest rates because they influence:

- Stock valuations

- Dividend stocks

- Bond markets

- Real estate investments

Many UK investors now view interest rate expectations as one of the most important market drivers.

What Experts Are Predicting

Forecasts remain mixed.

Some analysts still expect gradual rate reductions over the coming year if inflation moderates.

Others believe global energy market disruptions could delay cuts and potentially keep rates elevated for longer.

The most realistic scenario currently appears to be:

- Slow and cautious policy adjustments

- No rapid return to ultra-low rates

- Continued focus on inflation control

Key Takeaways

UK Interest Rates Remain at 3.75%

The Bank of England has kept rates unchanged while monitoring inflation.

Inflation Still Matters Most

Future rate decisions depend heavily on inflation trends.

Mortgage Holders Are Watching Closely

Even small changes could affect monthly repayments.

Rate Cuts Are Possible But Not Guaranteed

Economic uncertainty means policymakers remain cautious.

Savers May Benefit While Rates Stay Higher

Current savings products continue offering stronger returns than in previous years.

FAQ Section

What are UK interest rates right now?

The current Bank of England Bank Rate is 3.75%.

Will UK interest rates fall in 2026?

Potentially, yes. However, future cuts depend on inflation, wage growth and economic conditions.

Why are UK interest rates so important?

They affect mortgages, savings accounts, loans, investments and business borrowing.

How do interest rates affect mortgage repayments?

Higher rates usually increase borrowing costs, while lower rates may reduce monthly repayments.

Will mortgage rates fall if the Bank of England cuts rates?

Mortgage rates often follow broader interest rate expectations, although lenders also consider market conditions.

How do higher interest rates affect savers?

Higher rates generally improve savings account returns and fixed-rate products.

What is the Bank of England inflation target?

The Bank aims to keep inflation near 2%.

Author Bio

UK Markets Today Editorial Team

UK Markets Today publishes finance, investing, business, property and economic news designed to help UK readers make informed financial decisions through clear and trustworthy analysis.

Disclaimer

This article is for informational purposes only and does not constitute financial, mortgage, investment, or legal advice. Economic forecasts and interest rate expectations may change. Always conduct your own research or consult a qualified financial adviser before making financial decisions.

CTA

Stay Updated on UK Interest Rates and Market Trends

Want the latest updates on mortgages, inflation, investing, stocks, business news and economic forecasts?

Follow UK Markets Today for expert analysis, UK market insights and financial guides designed for modern British investors and consumers.