Bank of England Base Rate Explained: Latest Changes and What They Mean in 2026

The Bank of England Base Rate is one of the most important economic indicators in the UK. Whether you’re a homeowner, saver, investor or business owner, changes to the Bank of England Base Rate can have a direct impact on your finances.

Thank you for reading this post, don't forget to subscribe!When the Bank of England adjusts the base rate, it influences borrowing costs, mortgage repayments, savings returns and overall economic activity. As inflation and economic growth remain key concerns in 2026, understanding how the Bank of England Base Rate works has become increasingly important for UK households and investors.

What Is the Bank of England Base Rate?

The Bank of England Base Rate is the official interest rate set by the Bank of England’s Monetary Policy Committee (MPC).

It acts as the benchmark rate that influences:

- Mortgage rates

- Personal loans

- Business borrowing

- Savings account interest

- Credit card rates

In simple terms, the base rate determines the cost of borrowing money and the reward for saving money.

Quick Answer

The Bank of England Base Rate is the interest rate used by the UK’s central bank to help control inflation and support economic stability.

Why the Bank of England Base Rate Matters

Changes in the Bank of England Base Rate affect millions of people across the UK.

When rates rise:

- Borrowing becomes more expensive.

- Mortgage payments may increase.

- Loan repayments can rise.

- Savings accounts often offer better returns.

When rates fall:

- Borrowing becomes cheaper.

- Mortgage costs may decrease.

- Economic activity can be encouraged.

- Savings returns may decline.

Because of these effects, investors closely monitor every Bank of England announcement.

How the Bank of England Base Rate Is Set

The Monetary Policy Committee meets regularly to review economic conditions.

The committee considers:

- Inflation data

- Employment figures

- Economic growth

- Consumer spending

- Global economic developments

Its primary objective is to keep inflation close to the government’s target level.

If inflation rises too quickly, the committee may increase rates to slow spending.

If economic growth weakens significantly, rates may be reduced to encourage borrowing and investment.

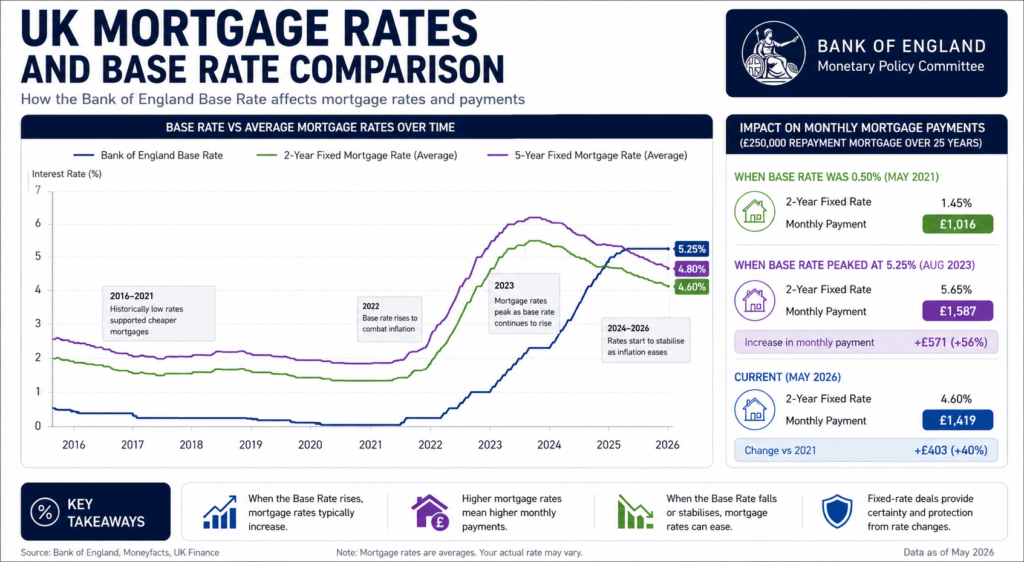

How the Bank of England Base Rate Affects Mortgages

One of the most noticeable impacts of rate changes is on mortgages.

Variable Rate Mortgages

Borrowers with variable-rate mortgages often see repayments change when the base rate moves.

Tracker Mortgages

Tracker mortgages directly follow the Bank of England Base Rate.

When rates increase:

- Monthly repayments rise.

When rates decrease:

- Monthly repayments fall.

Fixed-Rate Mortgages

Fixed-rate deals are less affected immediately, although future mortgage offers may change based on market expectations.

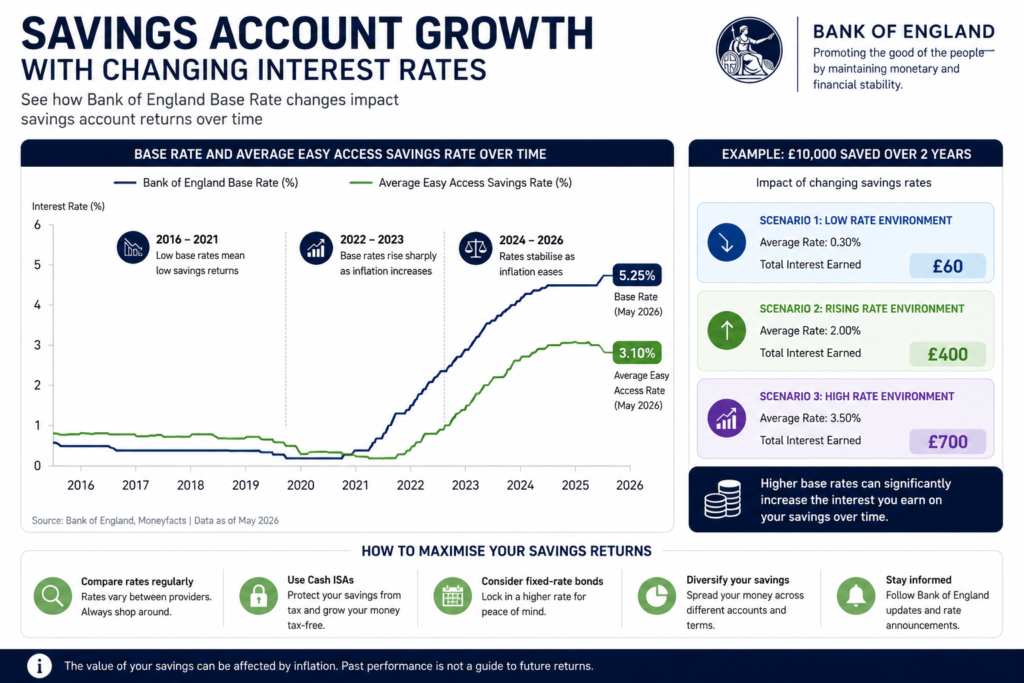

How the Bank of England Base Rate Impacts Savings Accounts

Savers generally benefit from higher interest rates.

Banks may increase:

- Savings account rates

- Fixed-term savings products

- Cash ISA returns

However, actual returns vary between providers.

Comparing savings products regularly can help savers maximise returns.

Effect on Businesses and Investors

The Bank of England Base Rate influences business activity and investment decisions.

Businesses

Higher borrowing costs can:

- Reduce expansion plans

- Increase financing costs

- Affect profitability

Lower rates may encourage investment and growth.

Investors

Interest rates often affect:

- Stock markets

- Bonds

- Property investments

- Currency markets

Many investors monitor rate decisions when evaluating portfolio risks and opportunities.

Bank of England Base Rate and Inflation

Inflation remains one of the main reasons the Bank of England adjusts interest rates.

How Higher Rates Help Control Inflation

When borrowing becomes more expensive:

- Consumers may spend less.

- Businesses may delay investments.

- Demand can slow.

This can help reduce inflationary pressures over time.

The Balance Between Growth and Inflation

Central banks must balance:

- Economic growth

- Employment levels

- Inflation control

Setting rates too high can slow the economy, while setting them too low may fuel inflation.

Recent Bank of England Base Rate Trends

Over recent years, the UK has experienced significant changes in interest rate policy.

Key drivers have included:

- Rising inflation

- Energy price increases

- Global economic uncertainty

- Labour market conditions

These factors have led to increased public interest in Bank of England decisions.

Bank of England Base Rate Forecast

Many people search for a Bank of England Base Rate forecast when planning mortgages, investments or savings strategies.

While future decisions cannot be predicted with certainty, several factors are likely to influence policy:

Inflation Trends

Lower inflation could support future rate reductions.

Economic Growth

Weak growth may encourage policymakers to consider cuts.

Labour Market Conditions

Employment trends remain an important factor.

Global Economic Risks

International developments can influence UK monetary policy decisions.

Investors and homeowners should remember that forecasts can change quickly as new economic data becomes available.

How Investors Respond to Base Rate Changes

Different asset classes react differently.

Shares

Some sectors benefit from lower rates, while others may perform better when rates rise.

Bonds

Bond prices often move in response to interest rate expectations.

Property

Mortgage affordability can influence housing market activity.

Currency Markets

Interest rate decisions frequently affect the value of Sterling against other currencies.

Key Takeaways

- The Bank of England Base Rate influences borrowing and saving costs across the UK.

- Mortgage holders are often directly affected by rate changes.

- Savers may benefit when interest rates rise.

- Investors closely watch Monetary Policy Committee decisions.

- Inflation remains one of the most important drivers of interest rate policy.

- Future rate decisions will depend on economic conditions and inflation trends.

FAQ Section

What is the Bank of England Base Rate?

It is the official interest rate set by the Bank of England to influence borrowing, saving and inflation.

Why does the Bank of England change the base rate?

The Bank adjusts rates to help control inflation and support economic stability.

How does the base rate affect mortgages?

Variable and tracker mortgages often move in line with the base rate, affecting monthly repayments.

Do savings rates increase when the base rate rises?

Many savings products offer higher returns when interest rates increase.

Who decides the Bank of England Base Rate?

The Monetary Policy Committee (MPC) makes interest rate decisions.

How often does the MPC meet?

The committee meets regularly throughout the year to review economic conditions.

Can the base rate affect investments?

Yes. Interest rates can influence stocks, bonds, property and currency markets.

What is the outlook for the Bank of England Base Rate?

Future decisions will depend on inflation, economic growth, employment and broader market conditions.

Author Bio

UK Markets Today Editorial Team

UK Markets Today provides trusted financial news, market analysis, investing guides and economic insights for UK readers. Our goal is to help readers make informed financial decisions through accurate and educational content.

Disclaimer

This article is for educational and informational purposes only and should not be considered financial, investment, mortgage or legal advice. Interest rates and economic conditions can change. Always conduct your own research or seek professional advice before making financial decisions.

CTA

Stay Updated on UK Interest Rates

Want the latest updates on the Bank of England Base Rate, inflation, mortgages, savings and investing?

Follow UK Markets Today for expert financial analysis, economic news and practical guides designed for UK readers.